—

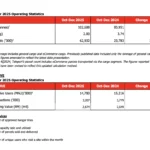

4Q2025: Capital A Companies (excl. aviation) revenue up 16% YoY to RM1.06 bil, EBITDA RM111 mil and NOP RM45 mil

FY2025: Revenue RM3.39 bil, EBITDA RM443 mil, NOP RM 171 mil

Positive shareholder equity of RM937 mil

Following the disposal of the aviation business to AirAsia X Berhad, the Group now comprises five core businesses—ADE, Teleport, AirAsia MOVE, Santan and AirAsia Next. Accordingly, this quarter’s results reflect aviation performance only up to 3 December 2025—the divestment completion date—covering approximately two months for 4Q2025 and 11 months for FY2025.

On a pre-elimination basis, the Capital A Companies generated RM1.06 billion in revenue in 4Q2025, surging 16% Year-on-Year (“YoY”). Margins proved resilient, with EBITDA rising in tandem with revenue by 7% YoY to RM111 million and Net Operating Profit (“NOP”) declined 12% YoY to RM45 million, due to lower interest income. However, interest expense was almost halved from a year ago. Profit After Tax (“PAT”) came in at RM9.82 billion, due to the large one-off gain relating to the disposal of aviation assets.

For FY2025, revenue was RM3.39 billion, for an EBITDA of RM443 million and NOP of RM171 million.

Highlights of the AirAsia Aviation Group

With the disposal of the aviation business now completed, the Group will no longer present highlights for AirAsia Aviation Group from this quarter onwards.

Highlights of Capital A Companies

ADE

Revenue for the quarter was RM247 million, up 31% YoY and 11% Quarter-on-Quarter (“QoQ”)—ADE’s best quarterly growth yet. This was driven by 51% YoY higher revenue from base maintenance, while line maintenance revenue rose 18% YoY on a greater number of flights handled. Growth was supported by expanding work for third-party airlines such as Air France, secured in the preceding quarter, reflecting growing recognition of ADE’s technical capabilities. EBITDA surged 79% YoY to RM55 million, with margins holding steady at 23%. Higher consumables tracked hangar capacity and activity expansion, offset by lower staff costs from operational optimisation initiatives. NOP and PAT margins came in at 11% and 14% respectively, supported by strong topline growth, favourable forex during the period and lower interest expenses following principal repayments.

For FY2025, revenue reached a new high of nearly RM895 million, with EBITDA of RM205 million and RM93 million NOP, reflecting scale benefits and improved financial efficiency.

CEO of ADE Mahesh Kumar on the business outlook:

“ADE is entering its next phase of growth from a position of strength. We are finalising a USD100 million debt facility to strengthen our capital base and accelerate expansion beyond Malaysia into Thailand, the Philippines and Bahrain—anchored to AirAsia’s Middle East hub and opening access to Europe. In addition to scale, we are also building depth. As part of our workshop expansion, we are progressively enhancing component and engine-related expertise to capture higher-value work in the maintenance cycle. And with our training centre set to commence operations soon, we are also building the talent pipeline needed to sustain growth and position ADE as a leading regional MRO platform.”

AirAsia MOVE

Driven by the launch of the B2B business—which contributed approximately 55% of revenue—as well as continued personalisation initiatives, revenue in 4Q2025 tripled QoQ and nearly doubled YoY to RM300 million. Margins remained resilient, supported by minimal marketing spend under AirAsia MOVE’s unique social-led acquisition model, delivering an EBITDA of RM45 million and NOP of RM40 million. NOP margin also saw a significant 6ppts QoQ uptick due to lower interest expense. Excluding B2B, Flights transactions climbed 12% QoQ, while Gross Booking Value (“GBV”) rose 28% QoQ on higher average spend. Performance was underpinned by a market-leading ancillary strategy with attach rates 23% higher than peer OTAs. Flights also secured two major partnerships with VietJet and IndiGo to further diversify its portfolio. Stays continued to gain traction, with conversion improving to 2.3% from 1.9% a year ago, pushing transactions up 2% and growing GBV 18% YoY. Duty Free outperformed, with GBV increasing 157% YoY following the commencement of operations in the Philippines and Indonesia.

For FY2025, revenue exceeded RM641 million, with an EBITDA of RM84 million and RM65 million in NOP, resulting in PAT of over RM54 million and reinforcing AirAsia MOVE’s return to sustained profitability.

CEO of AirAsia MOVE Nadia Zahir Omer on the business outlook:

“This year, we will double down on content to drive user acquisition and conversion. By leveraging user-generated content and deeper community engagement, we aim to attract higher-intent users while optimising marketing spend. This will be enabled by continued investment in technology, including the development of our virtual concierge, to enhance the booking experience, thereby improving retention and lifting NPS. At the same time, we will pursue greater Stays growth by leveraging our flight-anchored flywheel, deepening hotel partnerships and launching more personalised bundles to increase attach rates and customer lifetime value.”

Teleport

Teleport closed 2025 strong with record operational performance in 4Q2025. The company moved its highest volume of 102,688 tonnes (+19% YoY) and 63 million parcels (+165% YoY) with a new daily peak record of 974,000 parcels. This drove revenue growth to RM367 mil in Q4 2025 +10% YoY despite a 4% decline in Asia-Pacific market yield. Profitability momentum continued in 4Q2025, with Teleport recording a NOP of RM5.2 million (+RM7.5 mil YoY). For FY2025, Teleport achieved its highest-ever total volume of 347,885 tonnes (+18% YoY) and 167 million total parcels moved (+99% YoY), driving total revenue to RM1.2 billion (+11% YoY). This growth validates Teleport’s unique asset-light model of combining passenger and freighter capacity of third-party airlines, AirAsia belly space and Teleport freighters to meet growing market demands for eCommerce. Furthermore, this strong finish contributed to a full-year NOP of RM18.6 million, a RM40 million turnaround from a RM21 million net loss in FY2024. Teleport’s return to profitability at all levels was driven by strict cost and margin discipline, as well as a reduction in finance costs following the successful refinancing of the Deutsche Bank loan in 3Q2025.

CEO of Teleport Pete Chareonwongsak on the business outlook:

“Returning to profitability in 2025 is a testament to our team’s discipline, the trust our partners place in us and proves that Teleport’s asset-light model can scale profitably. Moving 167 million parcels and delivering RM1.2 billion in revenue proves that our model works at scale. This operating improvement, supported by the refinancing of our debt and a clear focus on both cost and margin discipline, gives us a solid foundation to scale further.

As we enter 2026, the USD50 million in pre-IPO growth capital from HPS Investment Partners allows us to accelerate this momentum. While we remain mindful of shifting market yields and currency volatility, we are optimistic and clear about our goal of moving more global eCommerce with the same discipline that delivered positive earnings this year. By further integrating partner airline capacity with our own network, we are building a sustainable, global logistics infrastructure that has long-term earnings potential.”

AirAsia Next

AirAsia Next has evolved from a brand licensing vehicle into a fully operational company with dedicated teams, embedded capabilities—and soon, including fintech and loyalty—and its own growth roadmap. Revenue for 4Q2025 saw a seasonal uplift to RM63 million in line with airline peak travel period. EBITDA and NOP margins came in at 35% and 27%, moderating due to the inclusion of BigPay’s performance, higher staff costs relating to internal cost reallocations and an increase in marketing spend related to sponsorships. Despite this, PAT margin remained healthy at 22%, attributable to the company’s asset-light model.

For FY2025, revenue came in at RM246 million, up 540% YoY, for an EBITDA of RM118 million and an NOP of RM95 million.

CEO of AirAsia Next Dennis Lee on the business outlook:

“AirAsia Next is no longer just a brand vehicle. It is a fully built ecosystem anchored on the five pillars of brand, loyalty, AI, media and tech. We’ve put dedicated teams and real capability behind it with one clear objective—to scale the brand faster and smarter. This includes monetising the AirAsia brand beyond Asean through the AirAsia Blue licensing and extending it into lifestyle, including hotels. We are building an integrated fintech and loyalty platform to deliver a 360 solution for our licensees, with licensing income in turn channelled back into advanced technologies such as agentic AI. Ultimately, this is about creating a virtuous cycle that brings the brand to more people, and more people to the brand.”

CEO of Capital A Tony Fernandes on the business outlook:

“The completion of our aviation disposal is a huge moment for Capital A. We said we would restructure, we said we would regularise, and we’ve delivered. The gain from the disposal has restored the Group to positive equity of RM937 million, marking a clear financial reset. Now we look forward to PN17 uplift and drawing a firm line under the past few years.

What I’m especially proud of is that while we were fixing the balance sheet, we were also building the future. We met our internal targets for 2025 despite not having all our planes—proof that the progress is real and measurable. And our full-year results reflect this momentum. Profitability has returned, our businesses are gaining traction, and the numbers reflect stronger cost discipline across the Group.

We’re now ready to turn the page and begin our next chapter of growth with renewed focus on the five tech-driven businesses we’ve built with AirAsia DNA—low-cost, efficient and designed to disrupt. AirAsia MOVE, Teleport and AirAsia Next, in particular, have enormous potential for hockey-stick growth due to their asset-light nature. I have no doubt that, in time, our market cap will come to reflect the true valuation that these individual businesses warrant.”

For further information please contact:

Investor Relations : Communications :

Joanna Ibrahim Maryanna Kim

Email: joannaibrahim@airasia.com Email : maryannakim@airasia.com

For further information on Capital A, please visit the Company’s website: www.capitala.com

Statements included herein that are not historical facts are forward-looking statements. Such forward-looking statements involve a number of risks and uncertainties and are subject to change at any time. In the event such risks or uncertainties materialise, Capital A’s results could be materially affected. The risks and uncertainties include, but are not limited to, risks associated with the inherent uncertainty of airline travel, seasonality issues, volatile jet fuel prices, world terrorism, perceived safe destination for travel, Government regulation changes and approval, including but not limited to the expected landing rights into new destinations.

Release ID: 89184422

If you detect any issues, problems, or errors in this press release content, kindly contact error@releasecontact.com to notify us (it is important to note that this email is the authorized channel for such matters, sending multiple emails to multiple addresses does not necessarily help expedite your request). We will respond and rectify the situation in the next 8 hours.